Karpathy Joins Anthropic — and Polymarket Priced It at 74%

Karpathy + Jensen's multi-cloud Anthropic capacity + Polymarket at 74% are one story: AI labor, compute, and conviction repriced in the same week.

On Tuesday, Andrej Karpathy posted what he framed as a "personal update": he'd joined Anthropic. The tweet did 193K engagement — the second-highest non-evergreen X post of the week. The press immediately framed it as "OpenAI co-founder joins rival." TechCrunch, Axios, and CNBC all ran some version of the same story.

That framing buries the lede.

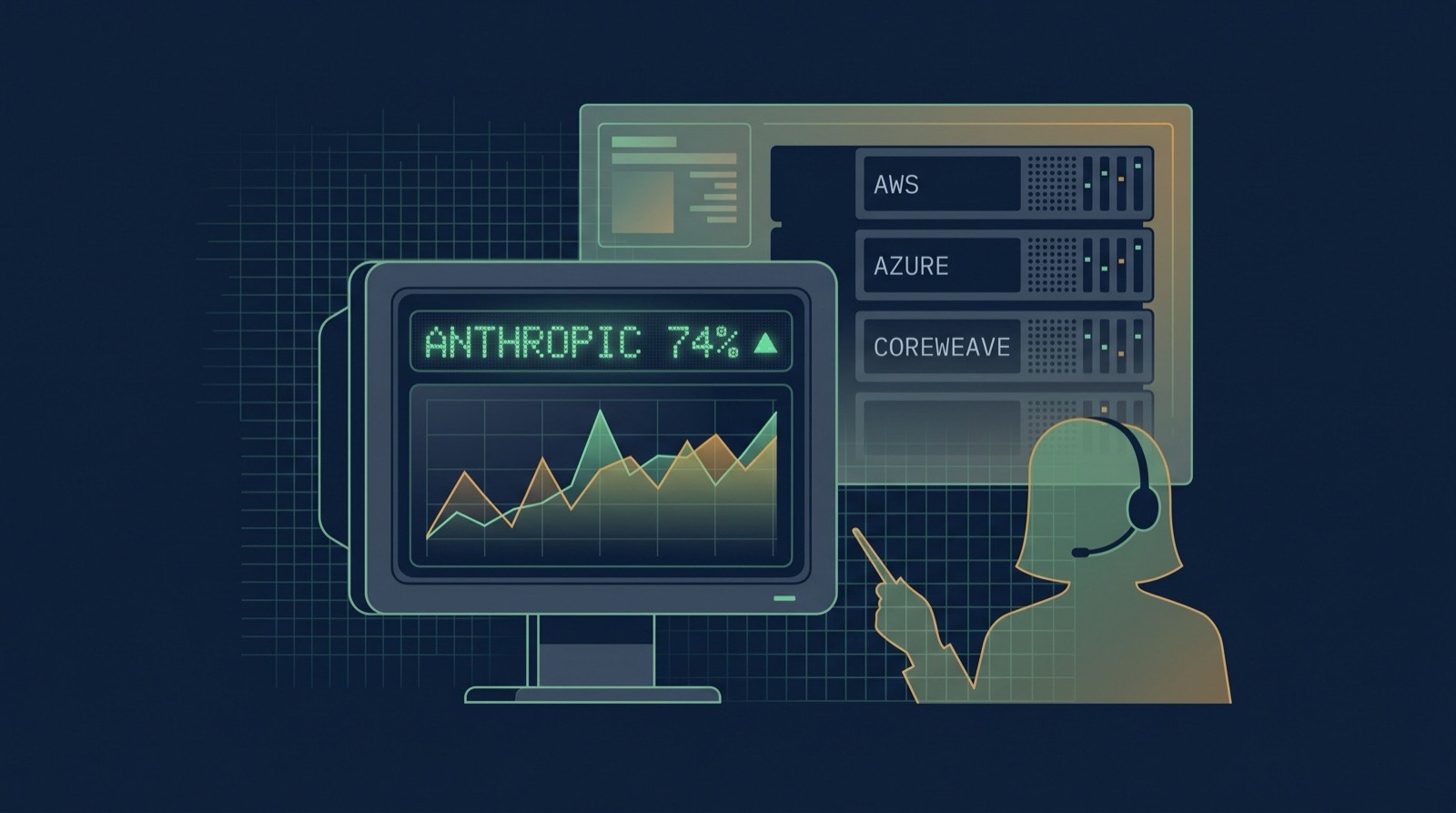

In the same news cycle, Jensen Huang stood on the NVDA earnings call and named AWS, Azure, and CoreWeave as the cloud providers building out Anthropic's capacity. Polymarket's biggest AI market — "best AI model end of June" — sat at Anthropic 74%, Google 24%, OpenAI 3%, with $1.62M of standing liquidity. Microsoft pulled Claude Code from a public deployment over budget overruns, and Chamath spent his morning tweetstorm calling it "the first, but not the last."

Three markets repriced in one week: labor, compute, and conviction. The hire isn't the story. The hire is the symptom.

What was actually announced

Karpathy is joining Anthropic's pre-training team under Nick Joseph. That's the team responsible for the foundational training runs that produce Claude. According to TechCrunch, he'll help launch a new effort focused on using Claude itself to accelerate pretraining research — Claude-on-Claude, the recursive self-improvement loop that every frontier lab is now racing to operationalize.

His own framing was deliberately small: "I think the next few years at the frontier of LLMs will be especially formative. I am very excited to join the team here and get back to R&D." That's the kind of statement an engineer writes. It's also the kind of statement that misdirects.

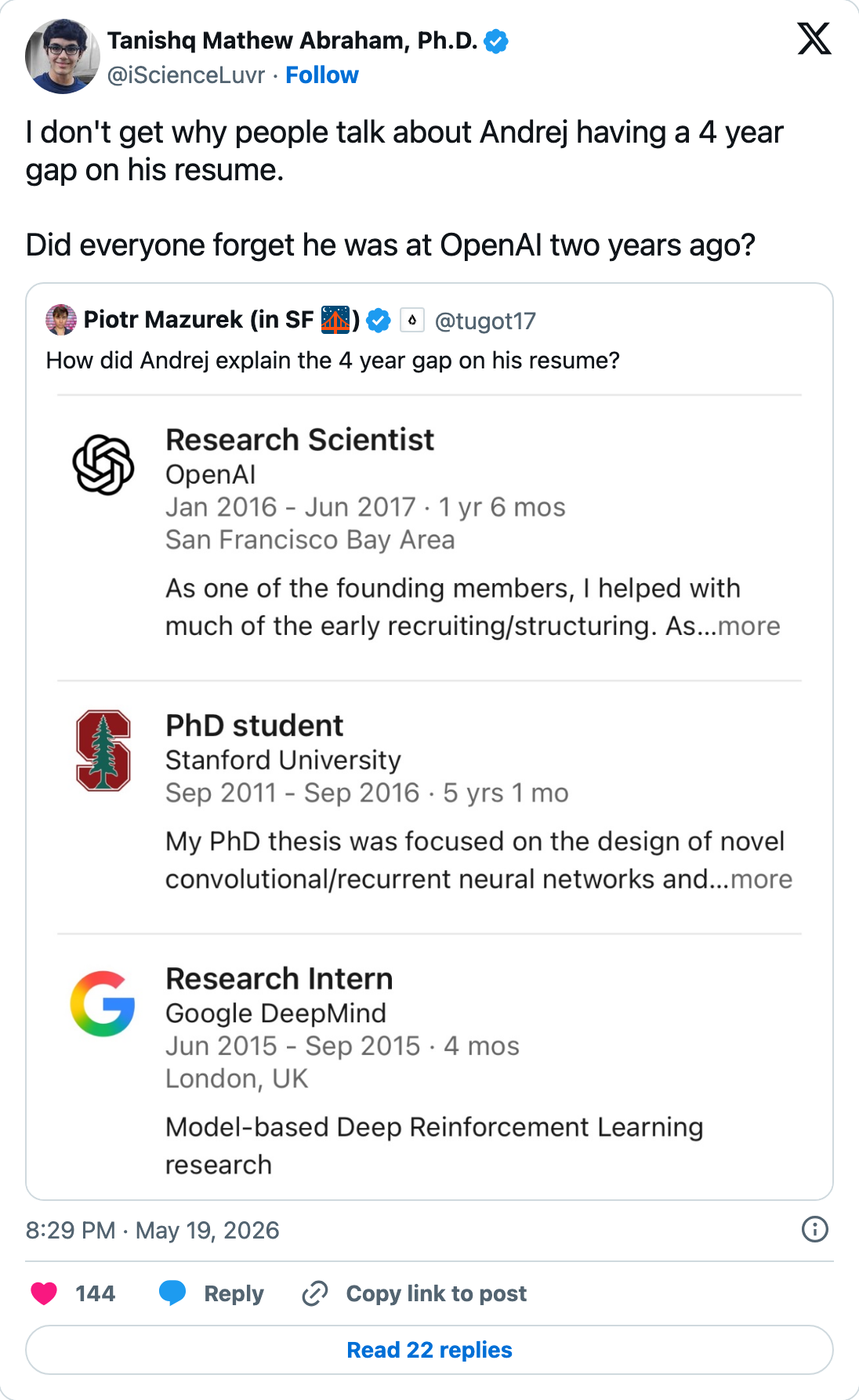

The AI-media memory is compressed to the point of revisionism. @iScienceLuvr cut through the "4-year gap on his resume" narrative with a single line: "Did everyone forget he was at OpenAI two years ago?" The answer is yes, mostly. Karpathy was a founding member of OpenAI in 2015, left for Tesla in 2017, returned to OpenAI in 2023, and left again in 2024 to start Eureka Labs. That's two departures and one return — and now a move to the competitor that was 1% of the prediction market three years ago.

The interesting question isn't "why did Karpathy leave Eureka Labs?" — solo educational labs are a hard business model. The interesting question is why Anthropic, now? The answer requires looking at the other two stories in the same news cycle.

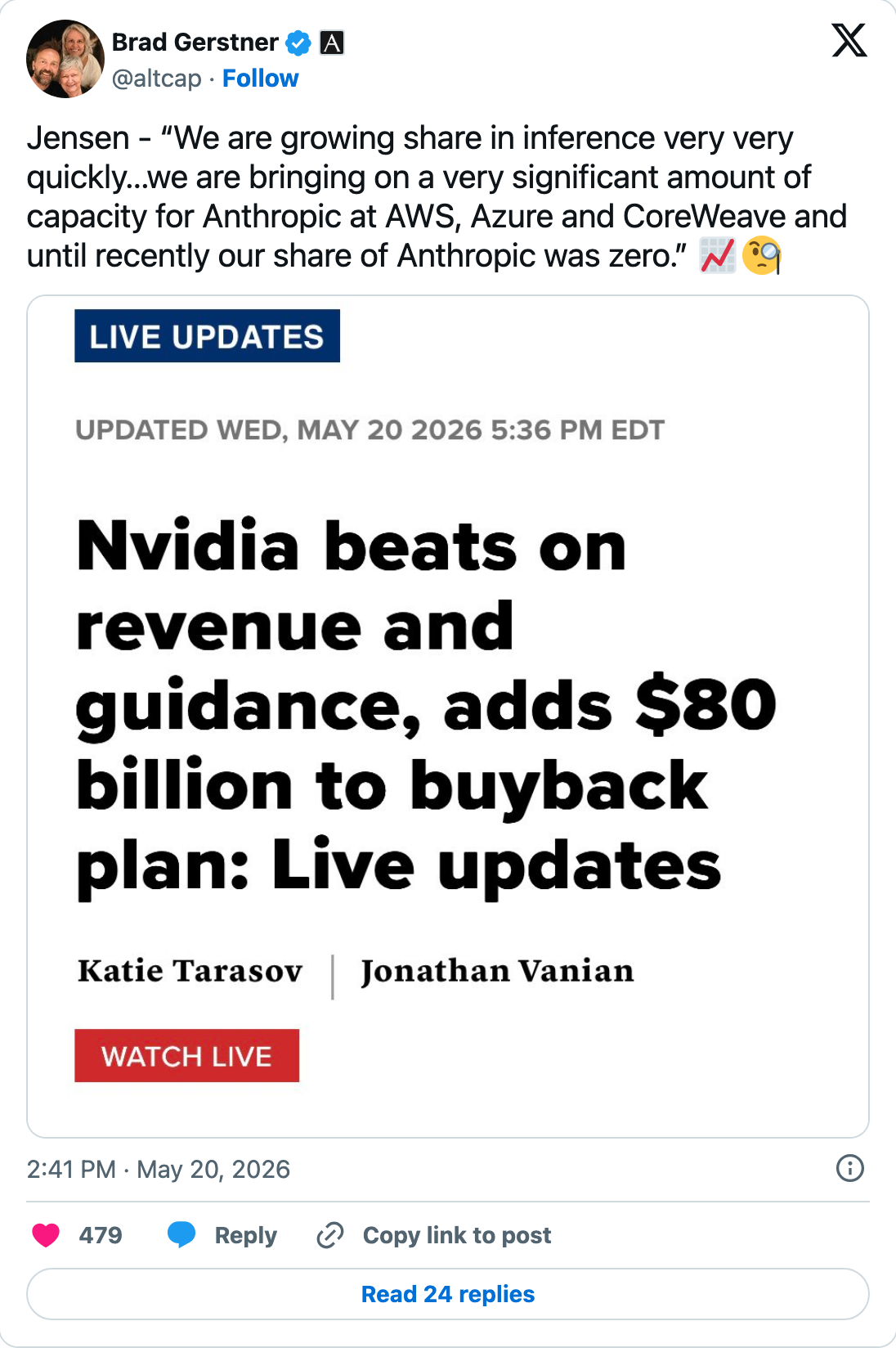

The compute side: Jensen names three clouds

On the May 21 NVDA earnings call, Jensen Huang said the quiet part out loud. Quoted by @altcap on X:

"...we are bringing on a very significant amount of capacity for Anthropic at AWS, Azure and CoreWeave..."

Read that list slowly. AWS, the platform of Anthropic's primary cloud partner and the $100B clock we covered last month. Azure, Microsoft's flagship — the cloud that has been the exclusive OpenAI substrate for nearly the entire ChatGPT era. CoreWeave, the NVIDIA-backed neocloud that has spent 2026 signing multi-billion-dollar deals with Meta and others to lock down GPU capacity through the early 2030s.

Three hyperscalers. One model lab. That's not a vendor relationship — that's a multi-cloud bet that mirrors the way large enterprises have always insulated themselves from single-provider risk.

OpenAI cannot match that posture without breaking the Microsoft exclusivity that defined the last seven years of its business. Anthropic can — and just did. Karpathy's move and Jensen's compute disclosure landed in the same five-day window. That is not how coincidence works at this level of public market disclosure.

The market side: 74% is not a soft number

Polymarket's "Which company has the best AI model end of June?" sat Tuesday at:

- Anthropic: 74%

- Google: 24%

- OpenAI: 3%

The market is the largest-volume AI prediction market on the platform: $346.8K of 24-hour volume against $1.62M of standing liquidity. It is not thinly traded, and it is stable — not whipsawing on news. The end-of-May version of the same market is essentially resolved: Anthropic 98%, OpenAI 1%, Google 1%. We covered the broader prediction-market / Ramp / GitHub-mindshare convergence last week — but the new data point this week is that the June market didn't move when Karpathy's news dropped. That's the market saying we already priced this in.

A 74% conviction line on a deep, stable Polymarket book is harder to dismiss than a 74% poll number. Polymarket Pros are paying for exposure to this outcome. When the numbers don't move on what looks like a major news event, the market participants are telling you the news was already a known unknown — they were waiting for it.

The OpenAI leg at 3% is the most interesting part of the book. If you believe OpenAI is structurally below Anthropic in operator preference (and the Ramp + GitHub trending signals back this up) but you also think there is any version of GPT-next that lands before June 30, the 3% line is cheap convex exposure. The same is true in reverse: if you think Anthropic has actually overshot conviction and the next 30 days will close the gap, the 24% Google leg is the trade. Neither leg is the consensus, and that's the point — Polymarket is doing the job that AI-vertical analyst seats used to do: pricing structural shifts in real time.

The contrarian read: this is not a hire, it is a regime change signal

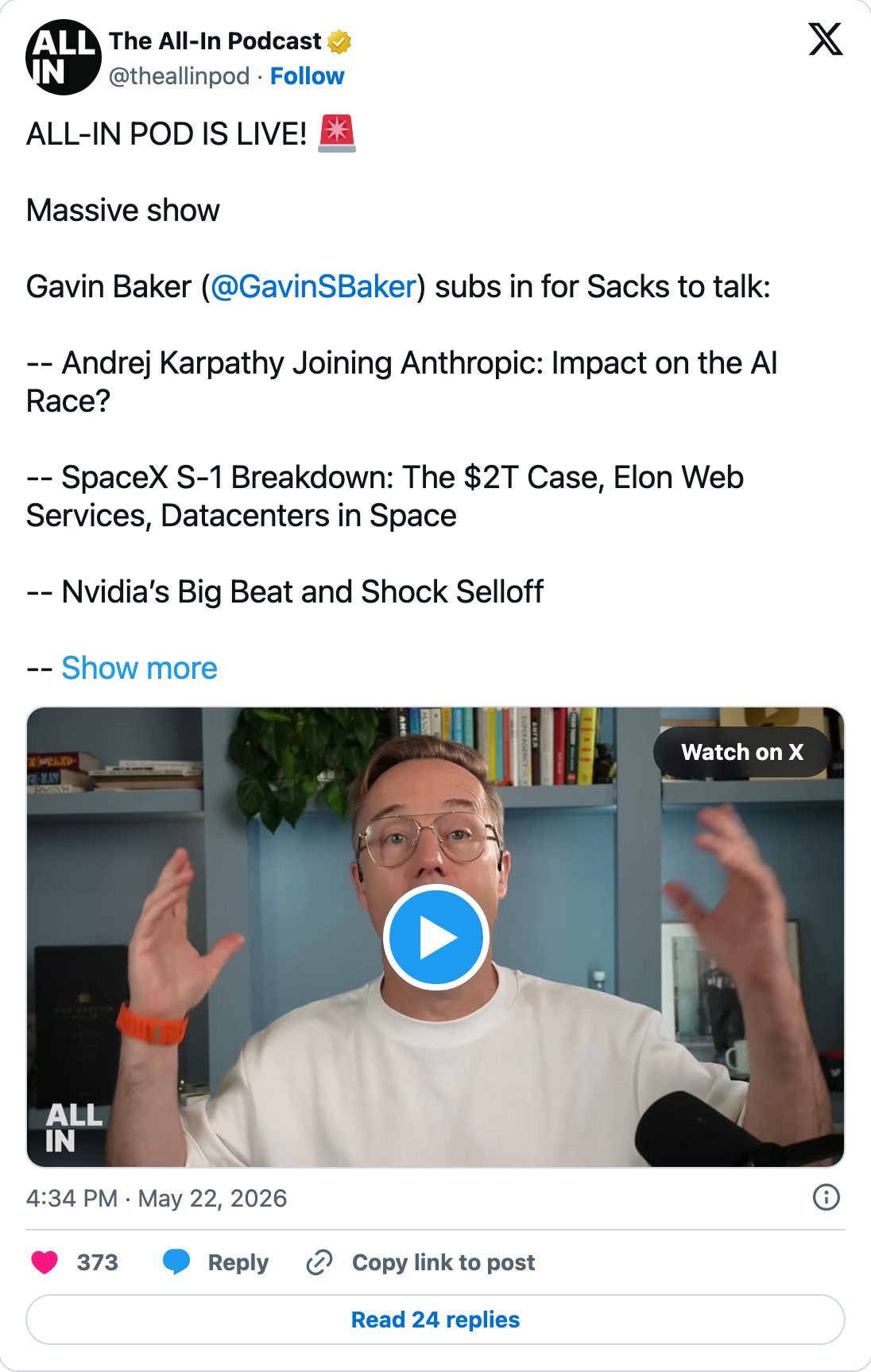

The All-In Podcast episode for the week paired Karpathy with the SpaceX S-1 filing. The episode title bills both together as "Impact on the AI Race." That's not a programming coincidence.

Sacks, Chamath, Friedberg, and Palihapitiya put Karpathy on the same episode tier as the most-anticipated tech IPO of the decade. They are telling you the move is a platform-class event.

Sacks, Chamath, Friedberg, and Palihapitiya put Karpathy on the same episode tier as the most-anticipated tech IPO of the decade. They are telling you the move is a platform-class event.

Read forward, not back:

- The compute story closed first. Anthropic locked AWS in October (the $100B deal), expanded to Azure and CoreWeave by May.

- The market repriced second. Polymarket's end-of-May resolution at 98% Anthropic is the prediction-market equivalent of a stock that broke out three months ago.

- The labor side is repricing now. Karpathy is the visible name. The invisible names — the second-tier OpenAI alums who quietly took meetings in Q1 — are the ones who will move next.

The contrarian forecast: a second OpenAI-alum hire announcement at Anthropic within 30 days. The labor market re-prices in waves, not in single events. The first wave (Karpathy) was the headline. The second wave will be the one that confirms the trend.

If that hire happens — and especially if it's somebody from the post-training or alignment side, where OpenAI's institutional knowledge advantage has been historically deepest — the June Polymarket market will move past 80%, and the 3% OpenAI leg will collapse to 1% within a week of resolution.

The second-order story: agent governance is the same story

Three other data points from the same week:

- Microsoft pulled Claude Code from an internal deployment over budget overruns. HN ran it as the #1 AI-tagged story.

- Chamath tweetstormed it as "the first, but not the last. The issue isn't that the tool isn't useful. The issue is that without context and oversight, the tool can spin forever..." link

- Anthropic shipped

/usagein Claude Code — a token-spend breakdown per Skill, Agent, MCP, and Plugin. That's an observability ship.

The thread connecting them: Anthropic just demonstrated, in real-time, that it sees the governance problem and has shipped the dashboard for it inside the same week that the news cycle pointed at the problem. That is exactly the move you'd expect from a lab that has just stacked compute, brought on a pre-training heavyweight, and is positioning to own the platform layer rather than win the next benchmark.

The companies that win the next 18 months of agent adoption will not be the ones with the fastest model on a cherry-picked benchmark — they will be the ones whose customers can prove to a CFO that the spend is bounded. Anthropic is acting like a lab that has internalized this. OpenAI is shipping Codex updates. Both are right strategies for different markets. The question is which market is bigger.

What operators should do this week

If you build on Anthropic. Treat the Karpathy + multi-cloud + market-conviction stack as durable, not a short-term news bump. Lock in the rate commitments that make sense for your 12-month roadmap. The compute side has structural redundancy now — Anthropic-on-AWS outages won't take you off Anthropic anymore.

If you build on OpenAI. Your compute-tier risk just diverged from Anthropic's. OpenAI is structurally Azure-exclusive in a way Anthropic is no longer. That is fine if your workload is Azure-aligned anyway, but it is the kind of single-substrate dependency that a CFO will ask about by Q3. Have a Plan B answer ready.

If you build on both. Use this week to write down which workloads pin to which model and why. The June Polymarket market is a fair external anchor for that argument inside your own org — "the deepest external book has Anthropic at 74%" is harder to wave off than "I think Anthropic is better."

If you trade. The OpenAI 3% leg on the June market is the cheap convex option, not the consensus. The Google 24% leg is the contrarian play. The Anthropic 74% leg is doing the work that being long the consensus usually does — capital-efficient, not capital-elastic.

Bottom line

The press calls it a hire. The market calls it a re-pricing. Both can be true, but only one of them is the structural story. Anthropic has now stacked, in a single news cycle: a marquee researcher, multi-cloud compute parity with the largest AI workload on the planet, a prediction-market lead that has stopped responding to news because it's already in, and a shipped observability dashboard for the governance problem the rest of the industry is still pretending isn't theirs.

Watch the next 30 days. The labor side hasn't fully repriced. When the second-wave hire lands, that's when the consensus catches up — and the trade is already filled.

ComputeLeap covers the platform-layer signals that define how AI infrastructure compounds. For prior context: Anthropic at 92% — prediction markets, Ramp, GitHub mindshare and the $100B AWS deal and the 6-month clock.

About ComputeLeap Team

The ComputeLeap editorial team covers AI tools, agents, and products — helping readers discover and use artificial intelligence to work smarter.

💬 Join the Discussion

Have thoughts on this article? Discuss it on your favorite platform:

Related Articles

Anthropic's S-1: What a $965B IPO Filing Changes

Anthropic filed its S-1 after a $65B Series H. What the confidential filing reveals about timing, AI capital risk, and the bull case.

Anthropic at 92%: Three Surfaces Tell the Same Story

Polymarket, Ramp, and GitHub trending all price Anthropic dominance. Where they agree, where they disagree, what operators should do.

Per-Seat SaaS Is a Liability: A 2026 Operator's Checklist

Palantir says SaaS is dead, Benioff calls it the third SaaSpocalypse, and HN is pricing the time bomb. Three failure modes and a buyer's checklist.

The ComputeLeap Weekly

Get a weekly digest of the best AI infra writing — Claude Code, agent frameworks, deployment patterns. No fluff.

Weekly. Unsubscribe anytime.